Below, we disclose our risk assessment model applied to each of our investment projects. The model follows a statistical process with automated appraisals. This model was developed by Moore Global, an expert in credit risk management models, in collaboration with WECITY.

Both Moore Global and WECITY have adopted sound governance mechanisms in the development of the rating, including internal controls and transparency procedures to ensure proper project management and oversight.

A distinction is made between three different analyses: the Developer, the Development and the Loan, each with a specific weight of 20% for the developer, 50% for the development and 30% for the loan in the overall rating. Within each of the three analyses, weightings are assigned based on different aspects, such that the maximum rating that can be obtained is 7.5 out of 9.

The remaining 1.5 points are reserved for evaluating various forms of project-related guarantees, with the first-ranking mortgage guarantee obtaining the highest score for the protection of our clients.

1 point: mortgage guarantee

0.5 points: pledge of the right to collect input VAT refunds

0.5 points: third party purchase option

This comprehensive approach allows for a detailed and fair evaluation of the fundamental aspects that affect the viability and security of investment projects. In addition, a macroeconomic analysis of the current situation of the country in which the development is to be carried out is performed.

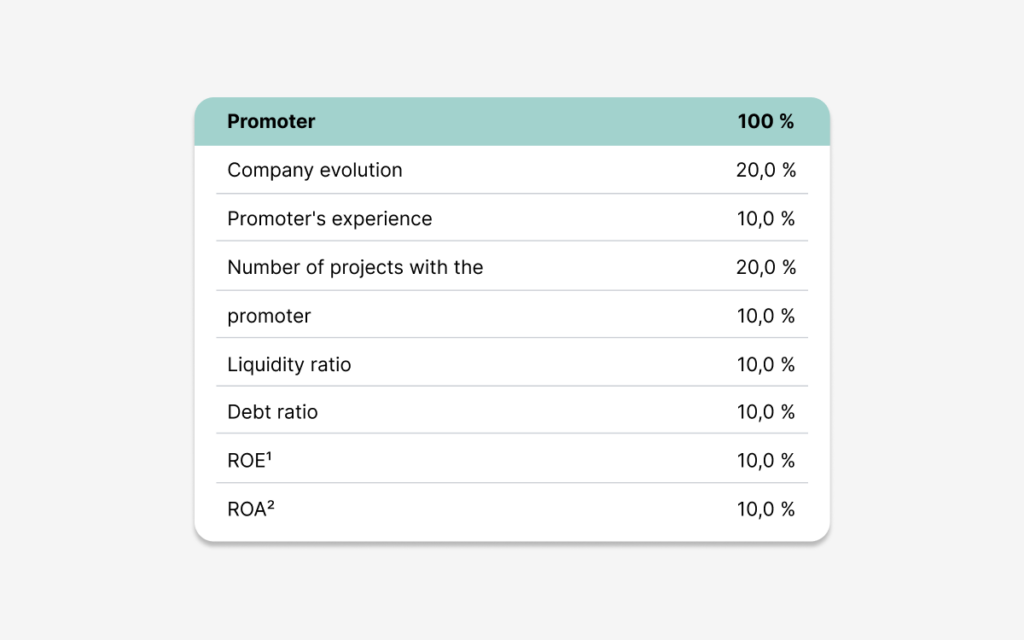

1. Promoter Rating

This first analysis focuses on the Developer that will carry out the development of the project. For the weighting, the model takes into account quantitative and qualitative information obtained from the documentation that WECITY. requests from the Developer and subsequently provides to Moore.

One of the aspects measured is the developer’s background in real estate management and development, as well as the stability of the project for which funding is requested, reflected in the corresponding ratios obtained from the financial statements. The model is NOT based on accounts that have been audited, except for a few exceptions in which the developers are obliged, by law, to carry out this procedure. However, the data is extracted from the tax returns filed by the developer, as well as from the Commercial Registry.

Additionally, the promoter’s experience is reviewed and it is verified whether it has been the subject of controversies in the past or if it has faced any problems in previous projects.

The documentation used comes from the Bank of Spain, the Mercantile Registry, the Tax Agency and the developer himself.

1 ROE: Return On Equity

2 ROA: Return On Assets

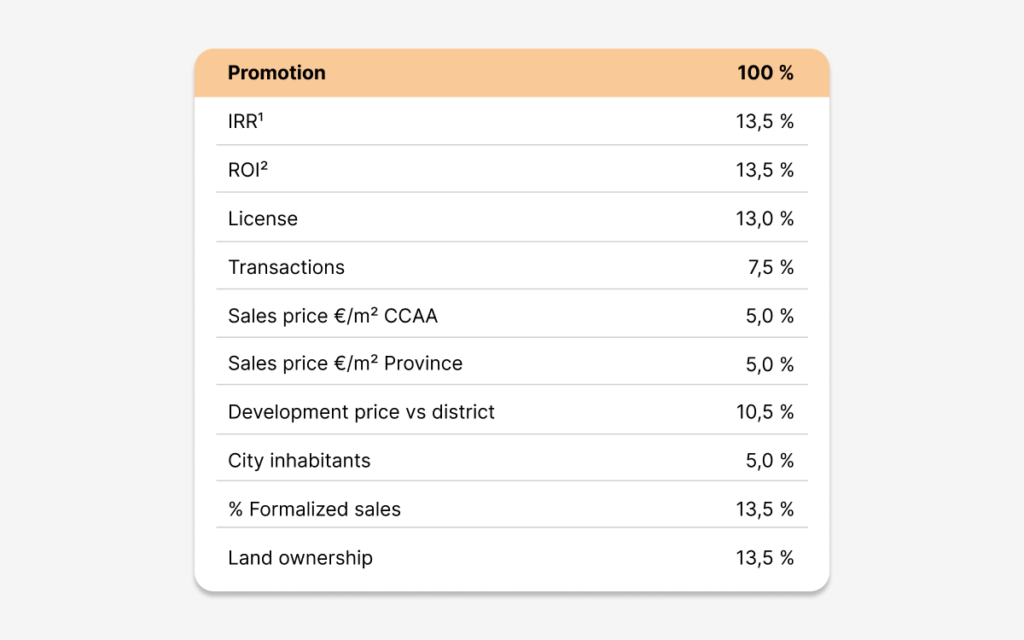

2. Promotion Rating

The second analysis is carried out on the project to be financed. On the one hand, estimates of financial results are measured -favored in the scenario where there is greater profitability and therefore greater return-, on the other hand, urban and legal risks -licensing and land ownership-, and finally, commercial risks -where the rate of sales, the price of sales, as well as the commercial status of the published operation are analyzed-.

1 IRR: Internal Rate of Return

2 ROI: Return On Investment

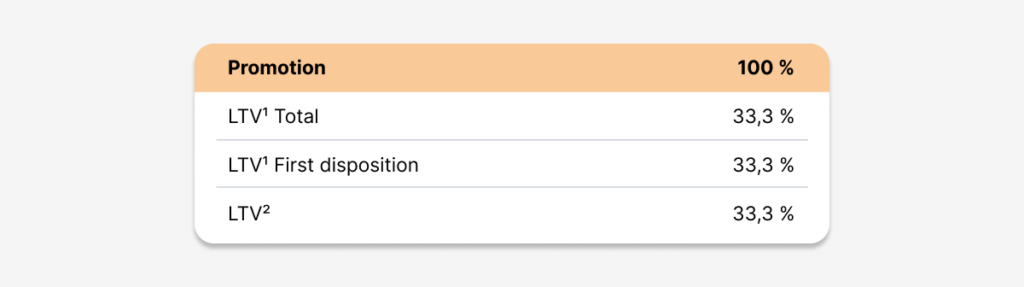

3. Loan Rating

The third and last analysis focuses on two fundamental ratios when making the decision to publish on the platform.

Firstly, Loan To Value1 is a ratio that measures the relationship between the loan and the value of the ECO3 appraisal of the asset issued by an approved appraiser. This value means greater coverage for the creditor in terms of loan repayment, the lower the value shown. It should be borne in mind that the appraisal offers present values (Current Appraisal) and future values (FT4 Appraisal). Depending on the object of the financing, either present values (acquisition of the asset) or future values (work; since the value of the asset increases as the execution progresses) are taken into account.

Secondly, Loan To Cost2 is a variable that measures the contribution of funds by Crowd investors with respect to the total costs of the project. As in the previous case, it is positively valued that the result of the formula is as low as possible, which translates into a high economic involvement in the project by the sponsor.

1 LTV: Loan To Value

2 LTC: Loan To Cost

3 ECO appraisal: in reference to Order ECO/805/2003, on rules for the valuation of real estate and certain rights for certain financial purposes.

and certain rights for certain financial purposes.

4 FT: Future Value

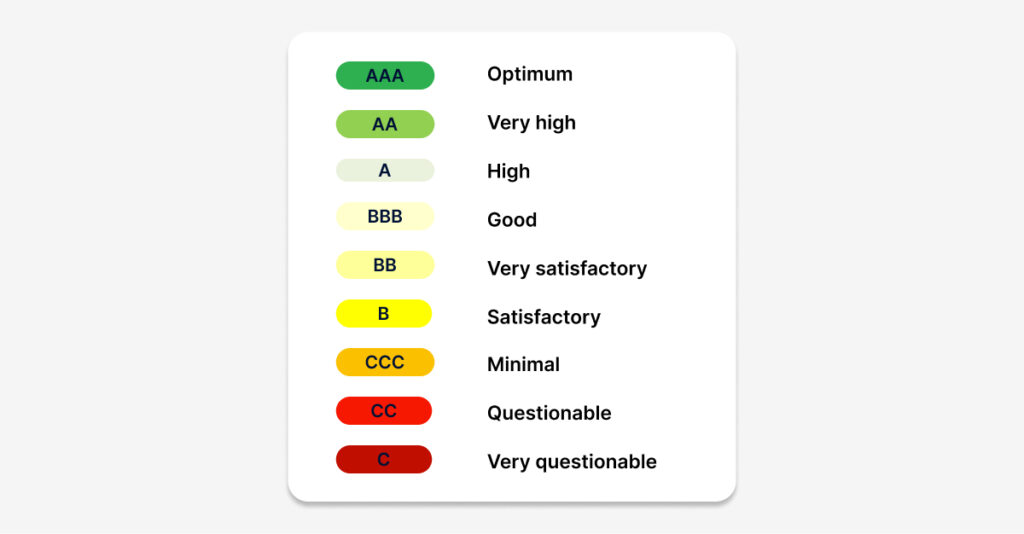

The rating considers 3 levels of investment quality:

Investments with optimal and high quality: AAA (optimal), AA and A (high).

Investments with good quality: BBB (good), BB and B (satisfactory).

Investments with minimal quality: CCC (minimal), CC and C (questionable).

With this risk model, WECITY. allows for a detailed and fair evaluation of the fundamental aspects that affect the viability and safety of investment projects.

WECITY. only selects projects with an optimal and high quality, those that have obtained a rating between A and AAA after the evaluation carried out by the model.